Natural gas heats eight in ten UK homes and provides one third of our electricity. Half of the gas we consume is imported, one-quarter of which arrives by ship in the form of liquefied natural gas (LNG), primarily from the US. The colossal $750 billion US–EU energy pledge will reshape global gas markets, with implications for UK energy prices and security of supply.

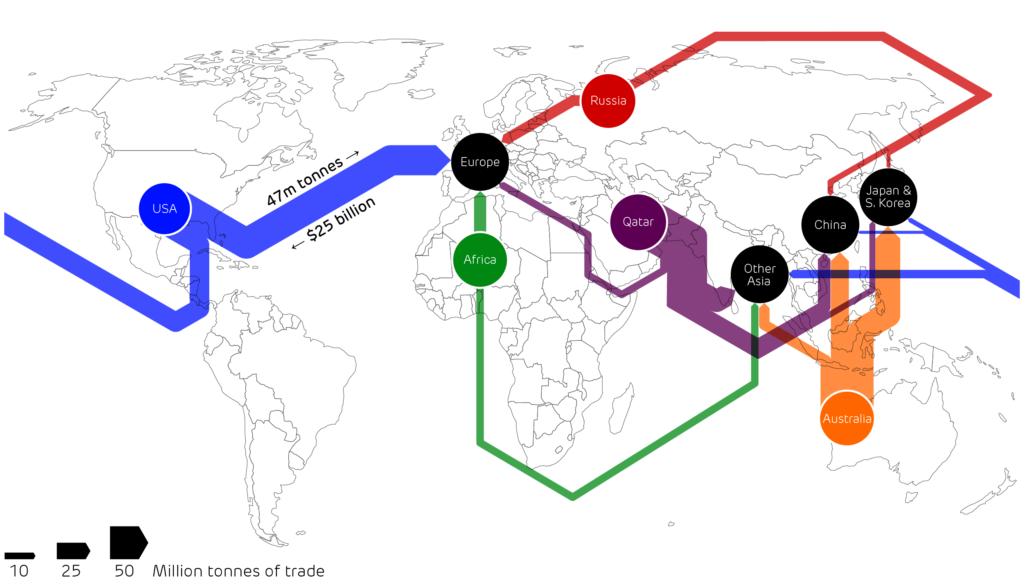

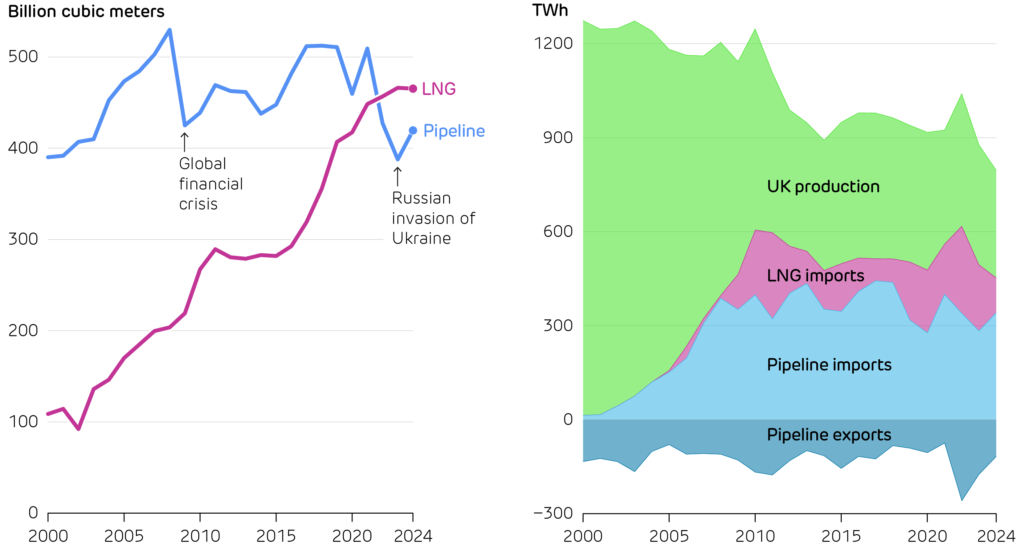

The UK’s dependence on imported LNG is a relatively recent phenomenon. The first ever LNG shipment came from Algeria back in 1964, yet by 2005 it still formed just 3% of the UK’s imports. Globally, LNG has now overtaken pipelines as the main form of trade, quadrupling from 140 to 550 bcm between 2000 and 2024. Qatar, Australia, and the US are the three major players in LNG trade. Qatar, home to the world’s largest gas field, started exporting LNG in 1997 and became the world’s largest source by 2010.Australia overtook Qatar in 2018, as exports from the Western Territory soared. It was not until 2016 that the first payload of LNG left the US, but export capacity has since increased twelve-fold (from 10 to 120 bcm), crowning it the world’s largest supplier.

The growth of major LNG exporters has been driven by breakthroughs in production and transport technology. Floating LNG enables offshore gas extraction without the need for expensive pipelines, while giant Q-Max tankers cut shipping costs by carrying over 3.5 TWh of cargo per trip (enough to heat 300,000 UK homes for a year).

LNG importers are concentrated in Europe and Asia. Production in the US flows to both continents, while Australia and Qatar cater primarily to the burgeoning Asian markets. Russian and North Africa export smaller volumes, mostly to Europe. Russian gas continues to enter Europe as LNG via spot diversions, worth around €8 billion per year. Russia accounts for around one-third of all LNG imported to France (8 bcm) and Spain (7 bcm) and almost half that in Belgium (3 bcm).

Left: Global trade in natural gas since 2000. Right: The UK’s source of natural gas since 2000.

Britain today is both a major LNG importer and a gateway to the Continent. Last year, most shipments arrived from the US (68%), with smaller amounts from Qatar (7%), Trinidad and Tobago (6%) and Algeria (5%). The UK’s three LNG terminals at South Hook (21 bcm/year), Isle of Grain (33 bcm/year), and Dragon LNG (8 bcm/year) could supply almost the entire UK’s demand of around 700 TWh per year. Some of this capacity is used to sell gas on into Europe: LNG is re-gasified in Britain and exported to the Continent via pipeline when European prices outrun those at home.

The new US–EU energy pledge is huge on paper, but bumps up against physical market limits. Europe cannot purchase, and US supply-chains cannot produce, the target $250 billion per year of energy. Total US energy exports amounted to ~$300 billion in 2024, with the EU accounting for just $80 billion. Replacing all Russian oil and gas imports solely with US supplies would increase Europe’s imports by around $70 billion over three years. That said, even a fraction of this volume would present a lucrative opportunity for Britain as one of Europe’s gas trading hubs.

Rising imports of US LNG to Europe will re-shape global gas markets, with first news of the US–EU energy pledge supressing UK gas prices. However, tariffs on US energy could have the opposite effect, driving up European and, indirectly, UK prices. Since gas sets electricity prices ~90% of the time, LNG price shocks feed straight into wholesale electricity costs. The UK must watch global gas geopolitics as closely as renewable energy goals. While Britain works to decarbonise its grid, flexible gas remains essential for meeting demand, and affordable LNG is key to maintaining supply-chain flexibility.

The major flows of LNG around the world. Arrow width is proportional to the annual trade in 2024.