Q3 2023: A sunny outlook for Britain’s solar power

Download PDF

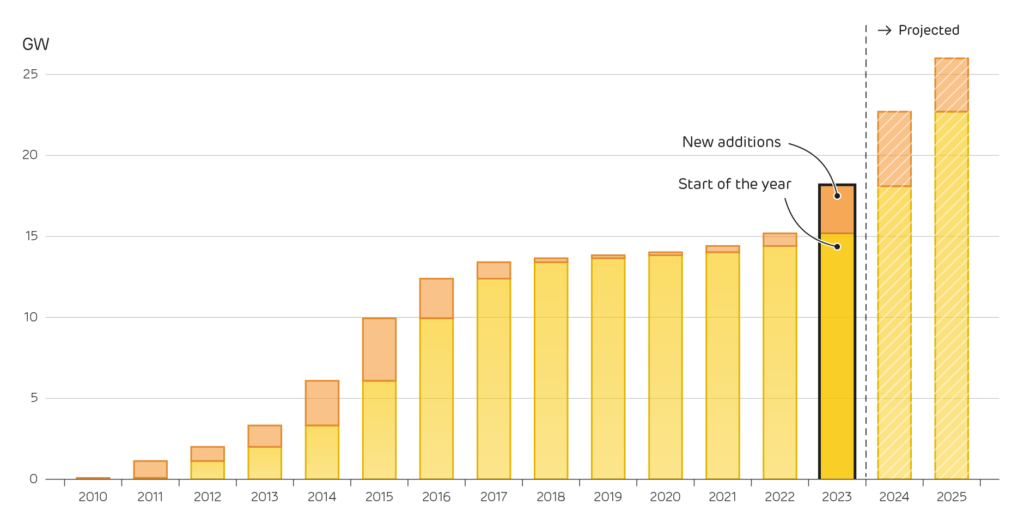

The rate of new solar panel installations has more than tripled over the last year. 2023 is set to see more capacity installed than the last six years combined. Next year Britain is forecast to install over 4 GW of PV capacity (1.5x the capacity of Hinkley Point C), and by 2025 total installed capacity is set to grow by more than 60%. Solar photovoltaics (PV) in Britain has been a story of boom and bust. Capacity grew rapidly a decade ago after lucrative feed-in tariffs (FiTs) were introduced in 2010. The rates on offer were soon slashed, and after 2015 the scheme collapsed. The Renewables Obligation (RO) scheme tells a similar story for larger ground-mounted solar farms. Rapid uptake from 2013, peaking in 2015 and then closure in 2017. Since 2019 almost all new solar PV has been without any policy support, and so installations were minimal. Solar capacity grew substantially across Europe last year in response to the energy price crisis and shortages of gas, and now that is catching on here. Falling prices for panels combined with high electricity bills make it worthwhile to install PV panels even without government support. This not only helps consumers to lower their bills, it also contributes to the country’s decarbonisation objectives. However, solar PV is not the easiest power source to manage. Solar output is highest on summer days, whereas demand peaks in cold, dark winter evenings. Both this seasonal mismatch and the strong day-night cycle of create issues with integration, and mean solar power is more likely to be curtailed.

Growth of solar power capacity in the UK since 2010, with projections from Rystad to 2025.

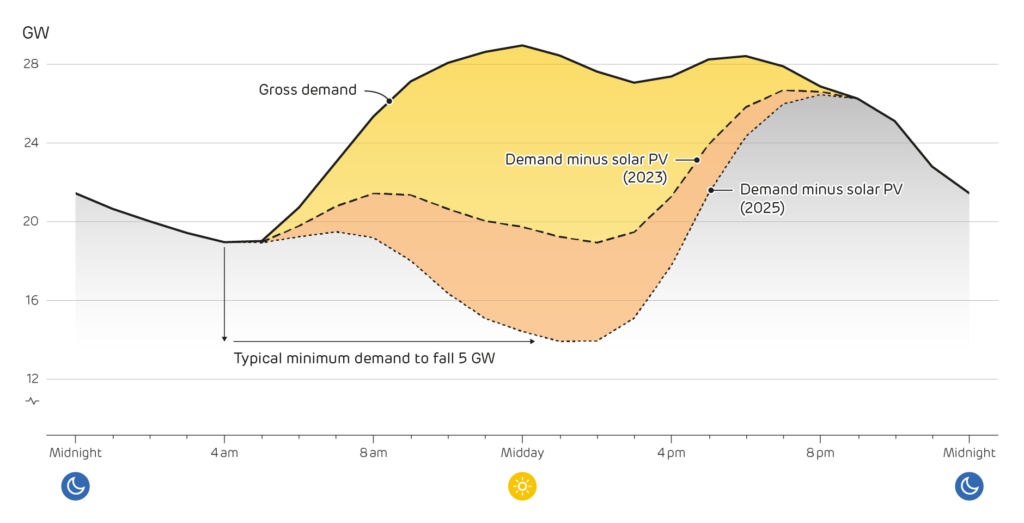

Currently, the sunniest summer weekends now see net demand in the afternoon fall to the minimums in the small of the night. But we are just now at the tipping point. Averaged over the ten sunniest days, net demand hit a minimum of 18.9 GW (typically at 2 pm), compared to 19.0 GW minimum for gross demand (at 4 am). But fast forward to the summer of 2025, we expect net demand on the sunniest afternoons will fall below 14 GW (5 GW lower than today), meaning 25% less space for other generators to operate.

This will crash wholesale power prices, as most of the country’s solar panels are not centrally dispatchable, meaning they export to the grid even when their power is not needed. The substantial negative power prices seen across Europe this summer will be a common feature in the UK too. Dealing with this effectively, and preventing renewable energy from being wasted, will require making the power system more flexible. More interconnection with neighbouring countries, and large-volume / long-duration energy storage will likely be key to managing the future power system.

The changing shape of Britain’s net electricity demand during sunny summer weekend days, due to growing solar PV capacity